The World Bank said Tuesday China's economy is expected to grow by 9 percent in 2005, and about 8 percent in 2006. In its quarterly update on the country's economy, the China mission of the World Bank said the economic outlook for China "remains good" in a stable macroeconomic environment and with favorable financial conditions.

OVERVIEW

China's domestic demand is slowing down. GDP growth remains high due to a large contribution of external trade as exports continued to power ahead while imports decelerated significantly. Net of external demand, the GDP numbers suggest that a slowdown in domestic demand is under way. Slower credit and profit growth, lower FDI and modest growth in machinery and equipment imports are pointing to a further slowdown in investment to a more sustainable pace in the period ahead. Signals are that the government's measures to slow the real estate sector are also starting to work.

The debate on the direction of the economy and the desired stance of economic policy is to some extend clouded by headline monthly activity indicators. Continued overheating, a soft landing, and the risks of deflation are all subject of recent debate. Indeed, growth in fixed asset investment and retail sales do not signal much of a slowdown. However, these numbers tend to overstate growth in investment and consumption, which are likely to have grown significantly less rapidly.

The change in the exchange rate system and the accompanying revaluation may further slow domestic demand. The impact on the trade balance is likely to be limited, but some of the capital flows associated with an expected revaluation could moderate in the months ahead, and therefore give the authorities more independence in conducting monetary policy. Development of forward markets to allow for hedging of trade and investment related capital flows is now a priority, as is close monitoring of short-term capital flows and exposure of domestic institutions to foreign exchange rate risk. Over time, more clarity on how the authorities will use their increased autonomy in monetary policy will become desirable.

China's macroeconomic outlook remains favorable, with some softening of growth expected this year, and some more in 2006. Risks have become more balanced. Downward risks include lower than expected export demand. A two-way risk is formed by the considerable uncertainty on the extent to which domestic demand, notably investment, is slowing.

While macroeconomic policymakers should remain alert to the possibility that risks materialize, for now the focus could be more on the structural issue of rebalancing growth. The rebalancing would be away from the relatively volatile export and investment-based growth to more stable consumption-based growth. Measures in social security and shifting government spending away from investment towards health, education, and social safety could help increase consumption's share in GDP, policies that would also help in redressing the surpluses on the current account. To maintain growth and employment creation as consumption increases, however, more efficient investment as well as a shift of investment to services is needed. Financial sector reforms, better corporate governance, and a dividend policy for state enterprises could be measures towards that goal.

RECENT ECONOMIC DEVELOPMENTS: DOMESTIC ACTIVITY SLOWING DOWN

National accounts and customs data suggest a slowdown in domestic demand in the first half of 2005. GDP growth remained high because of a large contribution of external trade. While it is hard to detect a domestic demand slowdown in the monthly activity indicators, these should be interpreted with care. Leading indicators point to a slowdown in investment growth to a more sustainable pace in the period ahead.

Real GDP grew a stronger than expected 9.5 percent in the first half. Nominal GDP growth slowed from 16.4 percent in 2004 to 14.2 percent in the first half of 2005. A strong contribution of net trade to GDP growth suggests a sizable slowdown in domestic demand in the first half. Although agriculture showed a strong 5 percent growth on the back of government subsidies and lower taxes, industry continued to outperform other sectors. Industrial value added rose by 11.2 percent in real terms in the first half of 2005 (year-on-year, (yoy)), which is consistent with strong external trade and moderating domestic demand. The rising share of industry in GDP to an unprecedented 59 percent raises concerns about environmental and resource constraints on growth as well on the sustainability of the current pattern of growth.

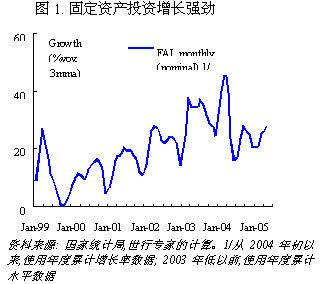

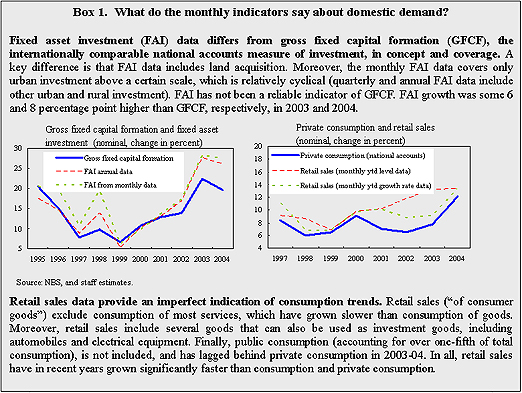

Fixed asset investment (FAI) growth, the target of the tightening measures in 2004, remained robust. It grew 25.4 percent (yoy), in nominal terms, in the first half of the year, more than in the second half of 2004, although significantly less than in end-2003 and the first half of 2004 (Figure 1). Based on recent experience, gross fixed capital formation, the internationally comparable national accounts measure of investment, is likely to have grown significantly less (Box 1). It is not easy to interpret the decomposition of nominal FAI growth in a volume and a price component.

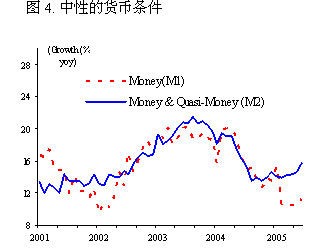

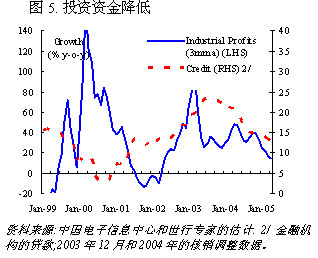

Key determinants of investment have slowed down, suggesting investment is heading for a more sustainable pace. Our econometric estimations indicate that FAI can be well explained by profits and credit growth, and both measures show signs of more moderate growth. M2 and credit, which decelerated during 2004, grew broadly at pace with nominal activity in the first seven months, suggesting a neutral monetary setting (Figure 4). Moreover, profit growth in industry has decelerated from 38 percent in 2004 to 19 percent in the first 6 months (Figure 5), reflecting strong competition and divergences between upstream and downstream price developments. Average profitability has leveled off across most industries, including in light manufacturing. In addition, utilized FDI has declined somewhat this year, and measures introduced to affect real estate investment appear to have had effect (see below).

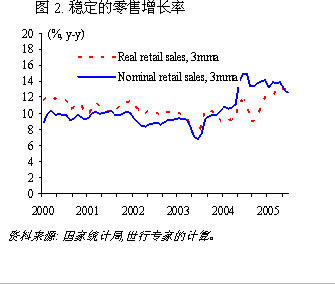

Real retail sales growth accelerated from 10.5 percent in 2004 to 12 percent in the first half, on the back of price declines for several consumer goods. They grew by 13 percent (yoy) in nominal terms in the first 7 months, the same pace as on average in 2004 (Figure 2). Retail sales, however, is an imperfect indicator of the national account measure of consumption, and has typically overestimated consumption growth (Box 1). Household survey data suggests that urban per capita living expenditure increased 7.6 percent in the first 4 months of 2005 (in nominal terms), suggesting significantly less growth in total private consumption than the retail sales data do.

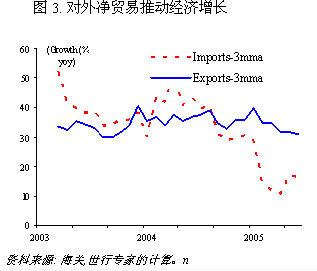

Net trade contributed strongly to growth. Merchandise exports were up by 33 percent (yoy), in US$ terms, in the first half, and by 29 percent in July (Figure 3). Textile and shoe exports to the US and the EU received headline attention, but these categories are growing more slowly than total exports. Import growth slowed to 14 percent (yoy) in US$ terms largely on account of mineral products, base metals, and machinery and equipment, and to 12.7 percent in July. Lower growth in machinery and equipment imports, from 33 percent in 2004 to 14 percent in the first four months of this year, is consistent with a slowdown in investment. The resulting turnaround in the trade balance of US$47 billion contributed over 40 percent of nominal GDP growth. The trade data may be distorted by over and under-invoicing due to expectations of RMB changes, although these distortions are unlikely to have increased so much in the first half of 2005 as to modify the conclusions based on the data.

Figure 1. Fixed asset investment robust

Figure 2. Retail sales growth solid

Figure 3. Net trade boosts growth

Figure 4. Monetary conditions neutral

Figure 5. Investment funding slowing

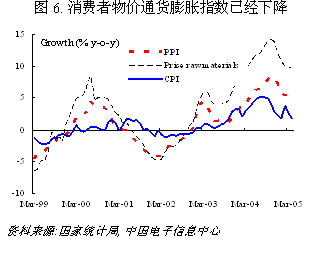

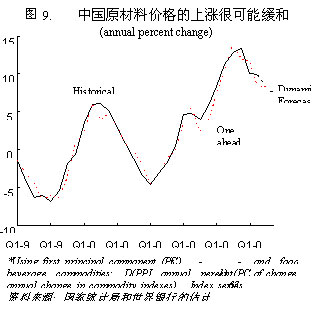

Figure 6. Consumer inflation has declined

Consumer price inflation has declined. Inflation came down from its peak of 5.3 percent in August 2004 to 1.8 percent in July, due to lower food price increases and price cuts in several industries where oversupply leads to tough competition, including clothing, household appliances, and transport and telecom (Figure 6). Increases in the PPI and raw material prices declined from their peaks of 8.4 and 14.2 percent in October 2004 to 5.2 and 9.0 percent in June.

THE ECONOMIC OUTLOOK AND RISKS

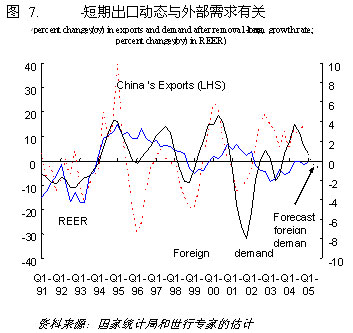

The macroeconomic outlook remains favorable, with some softening of growth expected. Growth in world economic activity and trade is projected to slow during the rest of 2005. World trade growth is now expected to slow from 12 percent in 2004 to 6.4 percent in 2005, which is likely to affect China's export growth (Figure 7).

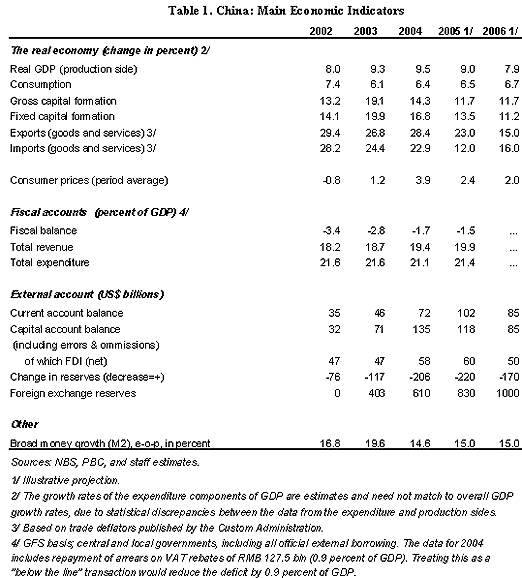

Exports will also be affected somewhat by the modest revaluation of the RMB and the recent measures designed to discourage exports of "highly energy intensive products", including the cancellation of rebates to exporters of VAT on aluminum and steel. Domestically, investment growth is expected to ease, reflecting the moderation in credit growth since the first half of 2004 and the more recent reduction in profitability and profit growth (Figure 5). In a stable macroeconomic environment and with favorable financial conditions, the outlook remains good, and we now project GDP growth of 9 percent in 2005, and about 8 percent in 2006 (Table 1).

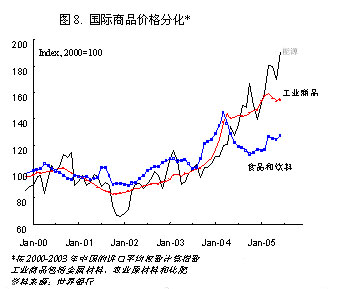

Price pressures are projected to ease. International raw material prices are generally easing, with the important exception of oil (energy) prices. Based on past patterns and the World Bank's international commodity price projections, increases in China's raw materials prices are expected to decline from 9.6 percent (yoy) in the second quarter to 7.3 percent in the fourth (Figures 8 and 9).

In addition, continued rapid productivity increases in China's manufacturing industry put downward pressure on prices. Finally, the recent revaluation will help ease imported inflationary pressures somewhat.

External risks appear modest. They include a larger than expected slowdown in world trade and new threats of trade protection against Chinese exports. In this connection, the changes in the exchange rate regime announced in July 21 should have a favorable impact on trade relations.

Enterprise profitability is at the core of domestic risks. One risk is that a moderation in profit growth will lead to a pronounced slowdown in investment, which will trigger a wider economic slowdown. While the recent strengthening of the RMB and likely associated effects on profitability are modest, expectations about possible future exchange rate movements could also affect investment. However, investment is unlikely to face a sharp correction, given the stable macroeconomic environment, underlying growth potential, and favorable financial conditions. Another risk is that investment is not reigned in sufficiently in industries facing potential excess supply and further pressures on profitability and prices, and that this would lead to oversupply, deflationary pressure, corporate sector balance sheet problems, and a new round of non-performing loans. This risk is real, given weak corporate governance and risk management.

ECONOMIC POLICIES

There are several tasks for macroeconomic and structural policy. Sustaining rapid growth means finding the right balance between preventing a sharp investment-led downward correction and, at least as important, avoiding excessive investment, deflation, and a large decline in profitability that would risk an even harder landing. While a more flexible exchange rate regime should eventually provide policymakers with more monetary independence to manage the domestic macroeconomic policy stance, in the immediate future careful management, including of expectations, is required. Reducing China's structural saving-investment surplus and increasing the role of consumption requires structural measures, including in public finance and corporate governance. Achieving these goals while keeping growth high also requires improving the allocation and productivity of capital alongside expenditure switching towards investment.

If deflation risks were to materialize, recognizing the cause is key for the appropriate policy response. Undue downward price pressures in some sectors are due to overinvestment rather than particularly weak demand. Consistent with recent price developments, our estimates -- based on growth accounting -- suggest that, with the structure of spending skewed to investment, the 9.5 percent GDP growth in 2004 was lower than potential GDP growth of almost 10 percent. Supply side driven deflation cannot be alleviated by easing monetary expansion and/or fiscal support along traditional lines, which would tend to encourage investment rather than consumption, thus potentially accentuating the problem. Rather, it requires a rebalancing of spending towards consumption, rather than investment, including via public finance reforms. More structurally, this also requires improvements in the efficiency of allocation of capital, via financial sector reform, improving corporate governance, and increasing dividends.

Corporate governance and dividend policies

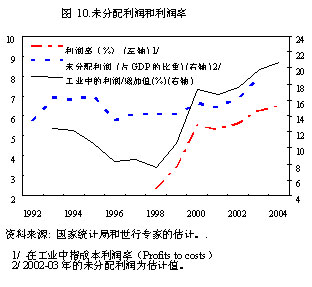

Improving corporate governance and increasing dividend payout would improve the efficiency of the use of capital and increase the role of consumption. These objectives have become more important as the profitability of Chinese enterprises has increased significantly and the role of retained earnings in financing enterprise investment has increased (Figure 10).

This is also the case for state-owned enterprises, where restructuring and the transfer of social responsibilities to the government have buoyed profitability. At almost 20 percent of GDP -- almost double the share in the US and France -- retained earnings finance the majority of enterprise investment. Given current corporate governance practices, investments financed by retained earnings may not always receive sufficient scrutiny. Strengthening the scrutiny with which earnings are allocated would tend to shift the trade-off between investment and consumption more towards consumption, as well as reduce the likelihood of "boom and bust" cycles caused by pro-cyclical profit-financed investment. The formulation and implementation of dividend policy is particularly appropriate for state-owned enterprises, which have not had to pay dividends to the shareholder since 1994, despite rising profits.

Fiscal policy -- key for increasing the role of consumption

Government revenues and tax revenues in particular have been buoyant in the first half of 2005. Net tax revenues went up by 13.4 percent (yoy), compared to a budget target of 11 percent for the year as a whole. Underlying tax revenues grew even stronger. Net tax revenues have been affected significantly by tax rebates to exporters. These were relatively low in the first four months of 2004. Taking into account the more rapid pace of tax rebates to exporters in the first half of 2005, compared to the first half of 2004, revenue growth was over 20 percent, with the key taxes -- VAT, income taxes -- all growing briskly, with no slowdown observable during the first half. Government expenditure increased by 15 percent (yoy), in the first half, compared to a target of 13.7 percent for 2005 as a whole. Prudent fiscal policy would imply not spending better-than expected budget revenues while growth remains buoyant. At the same time, looking ahead, the strong underlying fiscal position puts the government in a good position to use fiscal policy for macroeconomic management should the need arise, and to pursue important structural measures, including on the social safety net.

Fiscal policy can contribute significantly to increasing the role of consumption in the economy.

• A shift in government spending from investment to spending on health and education ("from construction of physical infrastructure to social infrastructure") would directly reduce national saving and investment in favor of consumption, in addition to supporting the drive to a harmonious society. The scope for such a shift is significant, given that current government financing of investment (directly and indirectly) is close to 10 percent of GDP.

• Particularly fruitful areas of structural fiscal reform are pension system reform so as to improve its financial sustainability, expansion of the social safety net and health care insurance, and clarification of the government’s role in financing of education. Currently, household savings appear to be affected by uncertainty as to future pension provision, and costs of health care and education. Removing this uncertainty and providing more insurance would thus support private consumption. If higher government spending is required to support these reforms, the current solid fiscal outlook provides room for important initiatives.

Monetary and exchange rate policy

Monetary policy has been complicated by very large balance of payment surpluses. Foreign exchange reserves continued to rise fast, reaching $711 billion at end-June, compared to $610 billion at end-2004. With much of the increase sterilized, domestic liquidity growth has not been excessive. However, the growing volume of outstanding central bank bills has changed the structure of the PBC's balance sheet rapidly, making it increasingly vulnerable to interest rate increases and capital losses on foreign reserves in case of exchange rate appreciation. Looking ahead, with inflationary pressure projected to ease further, and the recent revaluation implying a small tightening of the monetary stance, there does not appear a need for the PBC to counter the recent rise of money and credit growth, although high liquidity in the banking system remains a risk.

On July 21, the PBC announced a change in the exchange rate regime. The de facto US dollar peg was replaced by "a managed floating exchange rate regime ... with reference to a basket of currencies." The initial move entailed a 2 percent appreciation against the US dollar. The new arrangement uses a basket of currencies as a "reference", rather than a precise determinant, for the central parity that will be announced at the end of each previous trading day. The +/- 0.3 percent band has existed since 1994, but has not been used since the Asian crisis, when China decided to implement the de facto peg against the dollar that existed until recently. The band allows for the RMB to appreciate or depreciate a maximum of 0.3 percent per day. The PBC announced it would "readjust the exchange rate band when necessary.

The change in China's exchange rate regime represents a desirable move in the direction of greater exchange rate flexibility. Greater flexibility gives the authorities more room for maneuver in conducting independent monetary. At first, given the size of the balance of payment surpluses, the modest step towards more flexibility is not likely to reduce the exchange rate pressures by much, and the need for intervention and sterilization may remain substantial. Moreover, the modest appreciation will have only a small impact on the trade balance (Box 2 discusses the macroeconomic and distributional impact of a stronger exchange rate).

|

Box 2. A stronger RMB: macro economic impact and distributional issues

Together with a change in the exchange rate system, China revalued its currency by some 2 percent. A stronger RMB makes exports less attractive for Chinese firms, and makes imports cheaper. This decreases export growth and increases import growth. However, the size of these "expenditure switching" effects is relatively modest in China, limiting the impact of the revaluation on the external current account. A key reason is that the import content of exports remains high, despite the rapid broadening of domestic supply chains. Moreover, investment goods, raw materials, and intermediate goods make up the bulk of imports in China, rather than consumption goods. With the demand for these types of imports less price sensitive, expenditure switching towards imports is limited. Meanwhile, growth in investment, and thus overall domestic demand, is likely to decline as a result of weaker export growth and competitiveness associated with the stronger RMB that make investment in the tradable sector less attractive. The latter effect is likely to be relatively important in China. The dampening import growth resulting from lower growth of domestic activity would partly offset the reduction in exports and increase in imports because of the stronger currency. Thus, compared to industrial countries, expenditure reduction is likely to be relatively important, in comparison to expenditure switching.

We assess the economic impact with help of a macroeconomic model. The results of such simulations are only illustrative, since they depend on the model parameters -- assumed or estimated empirically -- including elasticities of exports and imports with respect to prices. Our simulations suggest that a 10 percent strengthening of the RMB would reduce GDP growth by about 1 percentage point in the first year and anywhere between 0.5 and 2 percentage point in the second. It would also reduce the current account surplus by 0.5 percent of GDP in the first year and anywhere between 0.2 and 1 percent in the second year, compared to a projected current account surplus of about 5 percent of GDP in 2005.1 While these number are only illustrative, they indicate that, given China's economic structure, an RMB appreciation large enough to eliminate the current external surplus by itself would have to be substantial, and would have significant impact on the domestic economy. Flanking a stronger currency with offsetting easing policies -- for instance, monetary or fiscal -- could dampen the negative impact on the domestic economy while increasing the impact on the external surplus.

In addition to the macroeconomic impact, the exchange rate change can have distributional implications. These largely occur via the impact of relative price changes on (the different components of) real incomes. An estimation of the impact on typical urban and rural households, based on the methodology of Chen and Ravaillon (2004) 2/, suggests that these effects are modest, though, as only moderate parts of household incomes and spending is affected by tradable prices. 3/ Urban households derive most of their income from wages, and some from net transfers and capital income. Thus, as long as the overall price level falls more than wages, which is probable, they are likely to gain somewhat from an appreciation. For rural households, wages account for a much lower share of income, and part of their cash crop revenue is affected by a decrease in the price of tradables. As a result, their real income is estimated to decline somewhat, despite the price decreases of their cash consumption. One caveat is that these results -- for "typical" households -- may not capture the full extent of the impact on poverty in rural areas. Marginal jobs in export industries are likely held by people coming from rural areas. Reduced activity in these industries as a result of a depreciation may slow down poverty reduction more than these numbers suggest. The distributional impact can be taken into account in the formulation of potential offsetting policy.

1/ The simulations were run with the standard Oxford Economic Forecasting model and with a modified version (with higher price elasticities in the trade equations and modeling an impact of foreign investment on exports), which gave the range of results.

2/ "Welfare Impacts of China's Accession to the World Trade Organization", in World Bank Economic Review, Vol. 18, No. 1. Their approach is applied here on a more aggregate level.

3/ For instance, estimations based on household survey data (from the NBS Statistical Yearbook) suggest that at most one-fourth of urban household spending is on tradables.

|

Indeed, with the initial revaluation smaller than many expected, speculative capital flows may actually intensify on the expectation of further strengthening. On the other hand, the "two way risk" associated with the new regime, the ambiguity about the composition of the exchange rate basket the PBC uses as reference, and the considerable daily variation that the PBC allows should discourage speculative inflows. In addition, with the increased flexibility, the PBC has the leeway to accept more of the incoming foreign exchange pressure by appreciation rather than intervention, if needed.

Early experiences with the more flexible exchange rate are encouraging for China. The non-deliverable forward rate fell briefly from 7.80 to 7.70 the day after the PBC announcement, but then recovered to 7.78 afterwards, indicating that

the 2 percent revaluation lowered expectations of further strengthening of the RMB. The exchange rate itself first further strengthened in the weeks after the PBC announcement, but then slid again to 8.109, perhaps in line with a weaker dollar against other currencies. Thus, the authorities seem to have stabilized expectations for further appreciation, while having demonstrated that there is, indeed, two-way risk.

Over time, more flexibility would make the associated advantages more pronounced. Monetary policy should become more independent; perceptions of two way risk should mitigate speculative capital flows; and the foreign exchange market should become deeper and more developed. However, as also indicated in Box 2, the exchange rate move does not remove the increasing structural imbalance between saving and investment that cause China's current account surpluses. This will have to be addressed by the structural policies discussed above, including improving corporate governance and increasing dividend payout, and shifting government spending to "social infrastructure".

Other economic policies

Concerned about real estate market developments, in May the authorities announced a set of measures aimed at curbing speculation, cooling down the housing market, and promoting construction of more low and middle-end housing. The real estate market measures include: (i) requiring local governments to ensure sufficient new construction of low and middle-end housing, capping real estate developers' fees, sanctioning developers for keeping land idle, and forbidding the resale of unfinished flats; (ii) requiring banks to tighten controls on real estate related lending; and (iii) taxing the (total) proceeds of the resale of new flats within two years. Earlier this year, the central bank also abolished preferential mortgage rates and recommended banks to increase the down payment required for a property purchase. Some cities also have implemented policies of their own, with Shanghai banning the transfer of uncovered mortgage loans and charging capital-gains tax on sales of houses that were previously sold less than a year earlier. These measures have had effect. Average property price increases declined to 8 percent in the second quarter (yoy), compared to almost 10 percent in the first.

The "go-out" strategy encourages overseas investment with an aim to secure natural resources and access to foreign markets and technology. As part of this strategy, the authorities have relaxed controls on overseas investment by releasing sector restrictions, abolishing the foreign exchange self-sufficiency requirement, and streamlining approval procedures. By end 2004, accumulated outward FDI had reached US$37 billion.

At end April, the State Council released its reform agenda for year 2005. According to this agenda, the reform priorities of this year cover ten areas:

• the rural economic system

• SOE and the management system for state assets

• the institutional environment for the non-public sector

• the financial system

• the fiscal, tax, investment and pricing systems

• establishing a modern market system of science and technology, education, culture, and health

• the systems of income distribution and social security

• the foreign-related economic system

• the administrative management system

It is expected that the forthcoming 5th plenary of the Central Party Committee of the 16th Party Congress this fall will further specify the key reforms in these areas, which will be implemented over the coming 11th Five Year Plan expected to be approved by the NPC next year March.

FINANCIAL SECTOR DEVELOPMENTS

China's financial sector reforms received a boost from foreign interest in the 4 State Commercial Banks (SCBs). Bank of America took a 9 percent stake in the China Construction Bank for a reported US$3 billion, whereas Singapore Government Holding Temasek announced plans to invest US$1 billion in the bank at the time of the planned initial public offering (IPO). Credit Suisse First Boston announced its interest in buying a stake in the Industrial and Commercial Bank of China (ICBC). Swiss bank UBS announced it may invest US$500 million in Bank of China, a bank that has also received interest from Morgan Chase, Royal Bank of Scotland, and Deutsche Bank. Meanwhile, Bank of Communications, a smaller state-owned bank, made a well-received US$1.9 billion IPO in Hong Kong in June. Last year, London-Based HSBC took a 20 percent share in Bank of Communications for US$1.75 billion. This foreign interest in China's banks is encouraging for the ongoing reforms in the sector which has long been fraught with policy-induced nonperforming loans that has resulted in repeated rounds of recapitalization starting 1999. The Agriculture Bank of China (ABC), the fourth SCB, has made no announcement regarding foreign interest. The bank has not yet announced a restructuring plan, and, unlike the other three banks, has not received a capital injection from government.

Strategic foreign investors are of particular importance for China's bank restructuring efforts, provided they can play a role in the banks' policy and strategy. This will depend on how corporate governance of these banks will evolve. Currently, for the recapitalized banks, Huijin, a company owned by the government, is exercising ownership. How this will evolve after the IPOs is yet unclear. For now, Chinese law restricts foreign ownership to 25 percent of equity, and 20 for a single investor. In the run-up to the IPOs of three of the four State Commercial Banks, restructuring efforts are under way, which is reflected in a decline in personnel and number of offices, as well as strong improvements in capital adequacy (after recapitalization) and rising profitability. Chinas' total banking sector recorded a profit of RMB93 billion last year, triple that of 2003. Some RMB65 billion of that accrued to the four State Commercial Banks.

The National Audit Office (NAO) reported to Parliament in July that in 2004 it had audited the 4 asset management corporations (AMCs) responsible for disposing of NPLs removed from the banking system. While the NAO praised the contribution of the AMCs -- Hua Rong, Great Wall, Orient, and Cinda -- to financial restructuring, it found that in 13 percent of the RMB 544 billion in assets audited (1/3 of the total assets held) irregularities were found ranging from procedural mistakes to fraud. ICBC, the latest SCB to restructure, disposed of some RMB650 Bn. RMB in NPLs through the AMCs and otherwise. With the transfer of non-performing loans (NPLs) to the AMCs, the capital adequacy ratio of the banking system as a whole has rapidly improved. However, the lending boom of 2003 and early 2004 may yet cause a rebound in that number, as the economy is slowing down, and some signs of overcapacity in several industries are emerging. Moreover, the presumably stronger SCBs have been losing market share in lending, while the generally weaker and less supervised local banks have gained it, which may have caused a weakening of the overall quality of loans that is yet to emerge.

The government's role in supporting housing finance is being debated. Although there is a general concern in China about overheating in the real estate market, there are also rising concerns that there is a lack of affordable housing at the lower end of the market. Traditionally dominated by banks, housing finance has taken off in China, with the stock of loans increasing to 11.7 percent of GDP in 2004. Further development of housing finance would be fostered by improving creditor information and strengthening financial risk management in banks. In addition, further financial market development would mitigate the challenges currently posed by funding mortgages with short-term deposits and the absence of a well-functioning secondary market. On the latter, the government initiated a pilot of secondary market development in early 2005 to explore better allocation of assets and capital of the banks by tapping into the capital market, with the first transaction scheduled to take place in the fall. It is important, though, to formulate a clearly defined overall public policy and strategy on housing finance, including the primary and secondary mortgage markets. An important part of this overall policy is to determine the appropriate nature of the role of government support to housing finance for lower and middle income groups, taking into account lessons learned in other countries.

CORPORATE SECTOR DEVELOPMENTS

CNOOC's now withdrawn US$18.5 billion cash bid for Unocal highlighted the urge in China to acquire overseas assets and create 30-50 globally-competitive enterprise groups. Press analysis mainly focused on political opposition in the U.S. There are, however, two more interesting developments: first, the comprehensive strategic nature of other recent bids and, second, potential links between outbound investment and reform of China's equity markets. Chinese enterprises excel at low-cost modular manufacturing (i.e., fitting into someone else's global supply chain), but have done less well in in-house R&D, industry standard-setting, brand development, global supply chain integration, and after-sales service. In choosing whether to "make or buy" these higher-value activities, it appears that out-bound Chinese firms are opting to buy. Lenovo's acquisition of IBM's PC business was a notable example of this.

China has recently seen moves to resolve the large "overhang" of non-tradable (NT) shares. Concern that the NT shares would be dumped on public markets helped spur a 50 percent decline in share indexes since 2001. The recent moves follow other earlier moves to empower minority shareholders -- which, for instance, gave CNOOC's independent directors a strong voice in reviewing the Unocal bid. In April, to encourage conversion of NT shares into tradable ones, the securities regulator suggested a post-conversion 3-year "lock up" for converted shares and required 2/3 of public shareholders to approve any conversion. Of the first two proposed conversions, one succeeded and one failed. To gain public shareholder acceptance, Sanyi Heavy's controlling shareholders had to provide additional free shares, agree to a longer "lock up," and set a minimum price for their eventual share sales. Thus, we've seen a market-based solution to a policy-induced problem. Another 42 companies have received approval to propose share conversion. The chief regulator indicated that lessons from this batch would soon be implemented in other listed SOEs.

Moves to empower public shareholders since late 2004 have been dramatic. Governance improvements should result in higher share prices. Higher share prices may make it financially easier for Chinese firms to acquire overseas firms through shares-only or cash-and-share bids, a common practice in western economies.

(China.org.cn August 17, 2005)